Iran Energy News Oil, Gas, Petrochemical and Energy Field Specialized Channel

Iran Energy News Oil, Gas, Petrochemical and Energy Field Specialized Channel

Related Articles

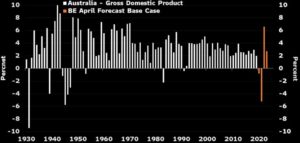

Australia appears to have succeeded in flattening the coronavirus curve, but such an optimistic health outcome won’t prevent the economy from experiencing a deep downturn. Our base case anticipates the largest contraction since the 1930-1931 Great Depression.

Significant stimulus — both monetary and fiscal — is cushioning households and helping businesses to survive and retain workers. Despite this, Australia’s small open economy has already seen considerable damage and faces headwinds from subdued global demand and trade. Significant monetary-fiscal coordination to provide further stimulus will be required to recover the economy over the years ahead.

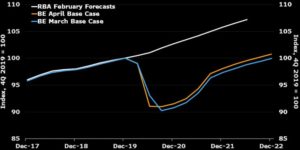

- We anticipate three consecutive quarters of declining gross domestic product, with Australia’s economy contracting by 9% from 4Q 2019 before a gradual recovery begins in 4Q 2020. We do not expect a recovery to pre-outbreak level of activity until 2H 2022.

- For 2020, our base case estimate remains a 6% contraction, unchanged from our previous projection. The better than expected virus containment would boost 2021 growth from 1.6% to 2.5%. A potential second wave of outbreak remains the main downside risk.

- Monetary policy has shifted to support fiscal policy and foster financial stability. The overnight cash rate is expected to remain on hold through at least 2022, with ongoing quantitative easing to contain yields amid rising issuance as fiscal packages and automatic stabilizers kick in.

- How far the unemployment rate rises depends on participation trends. Labor market slack is set to linger for years, which will depress wages growth and inflation.

Largest Financial-Year Contraction in Australian GDP in 90 Years

Australia’s apparent success in containing the coronavirus outbreak has paved the way for the economy to emerge early from an economic hibernation that was anticipated to last for six months. But this process is likely to be gradual, and won’t prevent a significant economic downturn.

Compared to our previous forecast, what has changed is the extent and timing of the hit to the economy from measures taken to confront the health crisis. There has been a significant pull forward of retail spending 1Q 2020. This will weigh on consumer spending in 2Q 2020, creating a deeper contraction then.

There is a non-trivial risk that the shopping splurge prevents Australia’s economy from contracting in 1Q, though we think this is unlikely given the possible declines in non-retail sectors of household consumption, and the broader economic activity.

We are now less confident in seeing the contraction in activity persisting through 3Q 2020. We currently anticipate a small fall in 3Q GDP, though this is highly dependent on how virus restrictions are unwound.

The lifting of restrictions will enable businesses to restart. But stoking demand may not be as easy given hits to household and business confidence, and damage to balance sheets. Resumption of economic activity will also be accompanied by some unwinding of temporary fiscal measures, which could dampen incomes and demand.

Recovery in Economic Activity Will Require Sustained Policy Support

As a small open economy, the weak global economic backdrop may also constrain Australia’s economic recovery. Further, risks of a second wave of outbreak —most likely imported — mean that restrictions on international travel are unlikely to be eased promptly. While Australia’s international borders will be kept closed for a further 3-4 months, the potential loosening of movement restrictions within virus-free zones, such as with New Zealand, does present an upside risk to the outlook.

Preliminary estimates from the labor market confirm that containing the virus has come at a great cost. Despite the substantial fiscal response, the grim reality is that not all businesses and jobs will be saved. Fiscal policy will need to pivot from economic survival to stimulus and recovery as virus gets under control.

The overhang in the labor market is likely to be more pronounced than traditional headline indicators suggest. Our forecast incorporates a sharp rise in the unemployment rate. But even still, the true picture of the shedding in labor demand, or degree of excess labor supply, is likely to be obscured by declines in participation and reductions in hours per employee.

As assistance payments taper and social distancing measures are gradually wound back, labor force participation, and subsequently the unemployment rate, is likely to rise. The significant dislocation within the labor market will probably linger for an extended period even though economic growth may bounce back. The economy will have to “run hot” — or above potential — for an extended period to not only re-engage unemployed workers, but to absorb underlying growth in labor supply.

This will weigh on already depressed wage growth for an extended period. In turn, prospects for wage-driven inflationary pressures are dim. Firms are unlikely to face a demand environment that’s conducive to lifting prices for some time. This will in part be compounded by households seeking to rebuild wealth through boosting savings, which risks postponing or muting the demand recovery. On balance, these forces mean monetary policy will remain accommodative for an extended period, in coordination with fiscal policy. The stronger and more sustained the fiscal response, the faster economies will be able to heal.

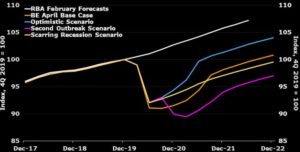

Australian Virus Recovery Scenarios

There are upside and downside risks to our outlook. Effective policy support in Australia, China and the rest of the world, could help the economy stage a stronger rebound. But the downside risks are considerable:

- Another flare-up of Covid-19 cases domestically could lead to Australia re-instituting another lockdown. Even assuming more moderate containment measures, the result would be a double-dip for Australia’s growth rate. We estimate that a second outbreak would prompt a contraction of around 3% in 4Q 2020, and lead to a contraction of 2.1% in 2021.

- The extent of any scarring: Even after a better than expected resumption of activity and significant government efforts, the lingering damage to the economy may prove greater than we have assumed. Damaged household and business balance sheets could crimp activity, resulting in a longer-than-expected recovery.

- On the upside, Australia could experience a better than expected containment and recovery. This could be further boosted by a potential twinning of Australia’s economy with New Zealand, which has experienced similar success in controlling the outbreak. The establishment of a trans-Tasman bubble which might experience more relaxed movement of people and activity could result in a stronger and and earlier recovery for both economies.

BE Short-Term Australian Forecasts With Scenarios